SMM, Oct 31, 2025 – China’s primary lead production edged down in October, dipping 0.56% MoM but rising 2.66% YoY. Cumulative primary lead output from January to October climbed 8.04% YoY.

According to the initial production schedules of primary lead smelters for October, output was expected to increase moderately as medium and large enterprises in central and north China resumed operations after maintenance. However, due to tight supply of lead concentrates, the pace of production resumptions in north China fell short of expectations. At the same time, unplanned production cuts at smelters in southwest and central China further dragged down output, resulting in a slight MoM decline.

Entering November, multiple primary lead smelters are set to resume operations following maintenance. Companies across central, north, southwest, and northwest China are restarting or continuing to ramp up production, which is expected to be the main driver of output growth this month. Although some smelters in east China plan to conduct equipment maintenance in early or late November, their relatively small capacity will not significantly affect the overall output growth forecast.

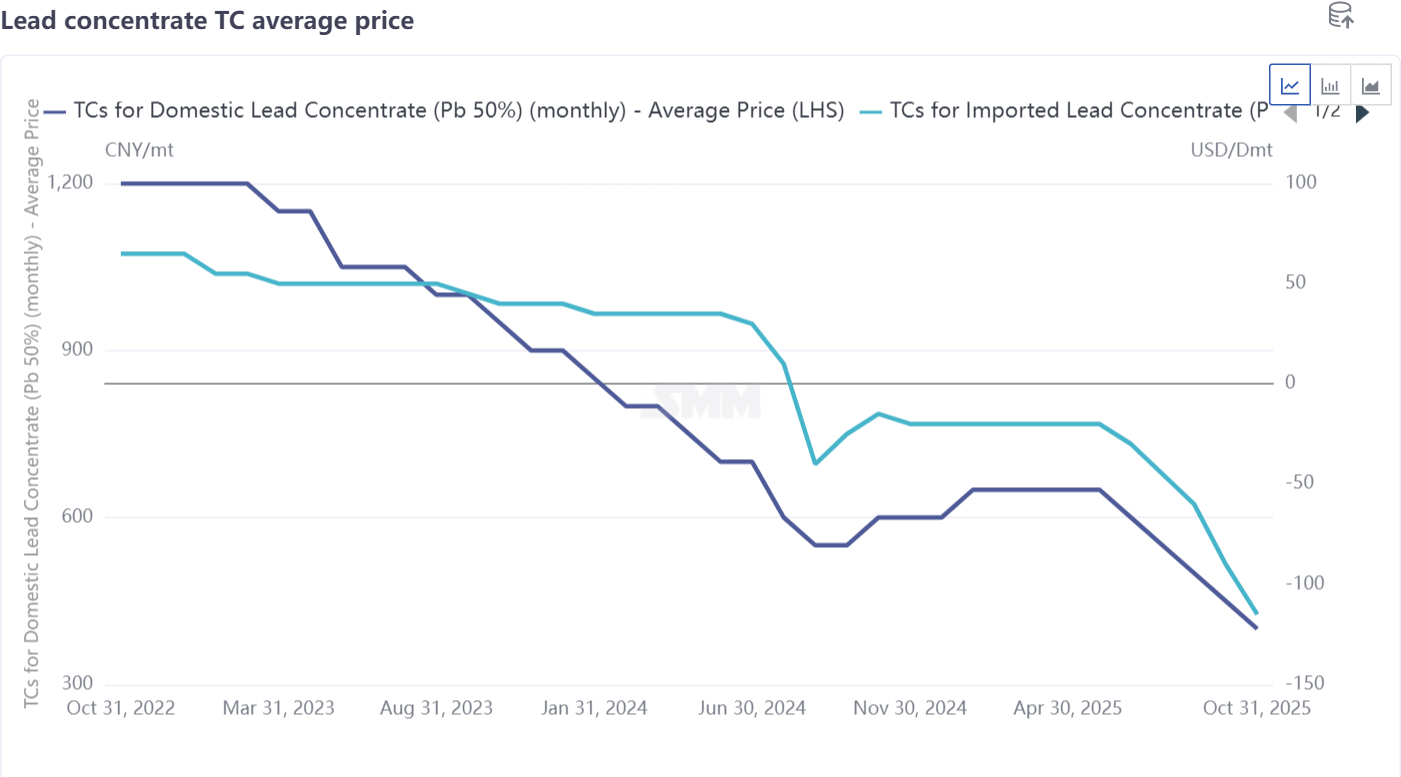

Nevertheless, the shortage of lead concentrates persists. Treatment charges (TC) for lead concentrates have been declining for six consecutive months with no signs of bottoming out, limiting smelters’ ability to raise output. On a positive note, import arbitrage for lead ingots opened in October, and refined lead also met import conditions. Some primary lead producers purchased imported crude lead, which is expected to partially offset the raw material shortage.

Overall, SMM expects primary lead production in November to increase by more than 2% MoM.

Data Source Statement: Data other than publicly available information are processed by SMM based on public information, market communication, and SMM's internal database model, and are for reference only, not constituting decision-making advice.